Explore the ScaleUp Annual Review 2021

Select a section to expand and explore this year's review.

CONTENTS

Introduction 2021

Chapter 1 2021

The ScaleUp Business Landscape

Chapter 2 2021

Leading Programmes Breaking Down the Barriers for Scaleups

Chapter 3 2021

The Local Scaleup Ecosystem

Chapter 4 2021

The Policy Landscape

Chapter 5 2021

Looking forward

Annexes 2021

Scaleup Stories 2021

2021 scaleup leaders’ views

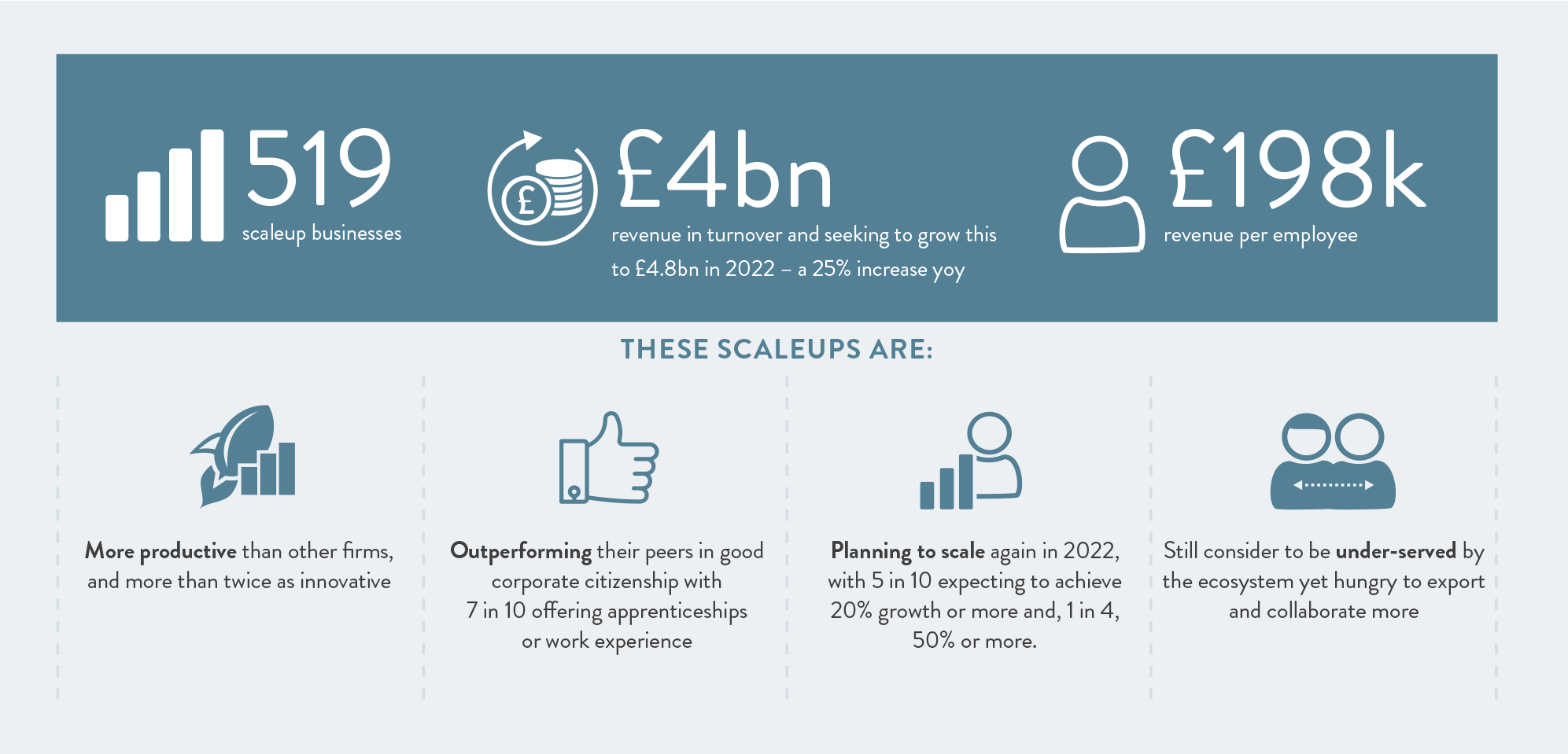

The 2021 ScaleUp Survey was completed by 519 scaleup CEOs. In this section we reveal the insights of our most ambitious scaling businesses, from a diverse set of sectors across the country, shining a light on the barriers they are facing while scaling up. Scaleup leaders remain ambitious with 9 in 10 expecting to grow their businesses even further in 2022 despite contending with ongoing challenges of Covid and new trading relationships with Europe, with 5 in 10 planning to scale up beyond 20% or more and 1 in 4 beyond 50%.

In the following pages we focus on the survey responses from scaleup business leaders whose companies are cumulatively generating £4bn turnover – a significant and diverse group.

In addition to rapid growth, scaleups are sizeable and often well-established companies. They remain highly innovative, international, and focussed on the future. Through the pandemic and in response to changes in international trade and the drive towards a greener economy they have pivoted and evolved, and are continuing to adopt new technologies and ways of working. They are focused on growth, on R&D (72% have invested in innovation and R&D), on moving into new markets (7 in 10 plan to export next year and over half already export) and on getting ahead in their current home market.

The 2021 ScaleUp Survey provides detailed and comprehensive insight into the issues that scaleups regard as vital to their future growth and development.

The key issues and barriers to further growth remain consistent with scaleup businesses continuing to grapple with access to markets, talent, and finance as their critical challenges as we head into 2022. Significantly, the talent challenge is dialling back up in 2021, whilst Access to Markets at home and abroad remain equally of concern.

Key Takeaways

- Scaleups remain resilient, ambitious and looking forwards – despite the continuing Covid challenge

- While the impact of the pandemic is perceived to be negative by 62% of scaleups, over the course of 2021 they have continued to pivot their business models, processes and practices, and increased their focus on innovation and R&D activity.

- They have utilised the different forms of support established, from Loans and Innovation grants to the Future Fund, and the Furlough scheme – showing the diversity of their size, scale and needs – and the importance of these interventions being made.

- There remains significant concerns on the path ahead. but leaders are feeling slightly more confident than last year that the UK will be a good location to do business in.

- Scaleups expect to grow, despite the ongoing effects of Covid-19 and the changing trading relationships with Europe.

- 9 in 10 scaleup leaders expect growth next year, with:

- 5 in 10 expecting to scale up their turnover and/or employee headcount again in 2021

- 1 in 4 expect this growth to be over 50%

- Turnover growth is expected by 9 in 10 scaleups in the next 12 months, while 8 in 10 expect to grow by employment.

- 4 in 10 scaleup leaders believe it is now harder to grow a business than it has been in the past with the same proportion worried that the UK will remain a good location for doing business. While those two factors have improved since 2020, slightly more 5 in 10 feel underserved by the business support on offer.

- 9 in 10 scaleup leaders expect growth next year, with:

- Scaleups are diverse – overall a third of scaleups (35%) has a female or ethnic minority founder, CEO or Board member.

- 33% of the scaleups responding to the survey had a female founder, 16% have a female CEO and 29% have women on the Board.

- 9% had a founder from a BAME / Ethnic Minority background, 4% CEO, and 7% represented at Board level. 20% have individuals from BAME / Ethnic Minority backgrounds in the wider senior leadership team.

- Reflecting current trends, 3 in 10 scaleups reported operating in the green economy (31%), and a similar proportion considered themselves a social business (29%), while 32% considered themselves ESG compliant (Environmental, Social and Governance). Overall, over half of scaleups (55%) felt they met at least one of these criteria.

- Scaleups are highly innovative. They are significant adopters of new technologies, and many work in partnership with others to develop new products and services, but they want more support.

- 9 in 10 have engaged in some form of innovation related activity: Three out of four scaleups have introduced a new or significantly improved product/process/service in the last 3 years. A similar proportion have invested in areas linked to innovation and 6 in 10 introduced significantly improved forms of organisation, structures and processes. 1 in 3 have undertaken innovative activities to meet green ambitions through reducing carbon output and energy consumption or improving environmental performance.

- Already significant users of collaborative tools, one in five scaleups are currently using big data or AI as part of their day to day operations. In the future they plan to further exploit these technologies for growth even more with 4 in 10 expecting to use AI, 3 in 10 big data, and 1 in 5 dialling up the use of robotics (21%).

- Growth is also being fostered through partnerships and collaborations with universities (37%), international partners (35%), large corporates (30%) and government (23%) to develop new products or services.

- Scaleups are very R&D focussed and accessing public sector funding for R&D is seen as the most vital support from the public sector (45%) alongside support from Innovate UK with 43% wanting easier access.

- Scaleups are focused on markets at home and abroad but issues surrounding market access remain pressing barriers for scaleup leaders

- Access to Markets continues to be the foremost challenge for our scaleups – 78% state that it is a vital or very important factor in their future growth, ahead of other barriers in 2021 as in 2020.

- Three quarters of scaleups primarily sell to other businesses or government (B2B) with 6 in 10 of them selling to corporates, while 24% of all scaleups sell direct to consumers (B2C).

- Collaboration rates remain low. Scaleups want to do more with corporates, universities and government with 4 in 10 aspiring to sell to corporates and 3 in 10 to government. Currently though collaboration rates remain very low – with only 3 in 10 working with corporates to develop a new product or service, it is a similar picture with Government where 2 in 10 have collaborated. 4 in 10 have collaborated with universities and research institutions.

- Scaleups are international. 57% of scaleups currently export – reinforcing the international nature of their footprint compared to SMEs generally. The EU remains their largest market but an increasing number are looking to other markets – 46% now trade with countries outside the EU continuing the increasing trend seen over the last few years. 65% of scaleups are seeking to engage in (more) international trade in 2022. They see key opportunities in North America, Australasia, the Middle East, China, India and other parts of Asia and overall, 62% aspire to export (more) to countries outside the EU.

- 1 in 3 now rates access to talent as their number one priority. Scaleups remain diverse employers but have some concerns over the future skills they will need to grow

- At 66%, access to talent is less likely to be rated as vital/important than access to markets but 33% of scaleups went on to nominate access to talent as their top priority for 2022.

- Scaleups are significant UK employers and it is worth noting that 47% hire people from the EU, while 36% hire people from outside the EU. Half of those currently employing overseas staff say it is very important that they continue to do so, while 5 in 10 of them agreed that it was vital/important to have access to the fast track visa system being developed by Government.

- Scaleups employ a wide range of people from interns to post grads and continue to demand a wide range of skills. Overwhelmingly scaleup employers rank critical thinking (70%) as one of the top three skills for their employees, followed by cognitive flexibility (44%) but they are less confident of finding either of these skills (30% and 29%), than they are of the third placed skill, service orientation (where 43% are confident of finding such employees).

- Scaleups want to help the next generation as they enter the workforce but are looking for support to take on new employees and ensure that they possess the right mix of skills and attributes. Given the range of people they look to employ, grant funding for training, apprenticeships and placements and changes in the ways in which educational institutions offer careers advice and entrepreneurial education all have an important role to play. Over 4 in 10 scaleups leaders are seeking to undertake more employer encounters with students. One in three are also looking for clearer forms of accreditation for digital skills.

- Amongst the senior leadership team, there is clear demand for skills around strategic and business development to support future growth, and a commitment to training the leadership team, but the local support offered by networks of peers, mentors and non-executive directors remains key.

- Finance and access to growth capital remains a priority issue for scaleups.

- They are far more likely to use external finance than their SME peers, 82% of scaleups use external funding as part of their growth strategy – yet 45% of scaleups do not feel they have access to the right funding for their needs.

- Perceptions of regional disparities persist with 41% of scaling companies in other regions continuing to feel that the majority of funding resides in London and the South East, compared to 20% among their peers in London and the South East. However, whilst scaleups in the North of England are somewhat less likely to currently be using equity finance (19%) there is little difference in use between those in London and the South East (30%) and those in other parts of the UK (from 24% in the devolved nations to 34% in the Midlands).

- Angels and VCs continue to be key early stage investors with 5 in 10 scaleups either currently having that investment or looking for such investors going into 2022.

- Scaleups value relationship management and being ‘put on the map’.

- Six in ten (63%) of scaleups would like a single point of contact to act as a relationship manager for them when dealing with the public and private sector.

- 64% of scaleup leaders want to be identified as a scaleup on public record on an opt-in basis. 5 in 10 would welcome the government sharing internally with other government departments that they were a scaleup or fast-growing company.

The Top Challenges

- Access to markets – both at home and abroad – continues to be the most significant issue in the 2021 ScaleUp Survey that our scaleup leaders are grappling with. Scaleups want greater opportunities to collaborate with, and the ability to sell into, the public sector and large corporates however barriers still remain. Not enough scaleups are getting the opportunities to supply to large corporates or work with Government. Collaboration rates remain extremely low with only two in ten collaborating with government, just three in ten collaborating with large corporates and four in ten with universities.The main barriers to collaboration scaleups continue to cite as needing to be resolved are time-consuming and complex procurement processes, and a lack of identifiable opportunities. Action and concerted effort is needed now to resolve these issues.For scaleups primarily selling direct to consumers the key barriers to their ongoing growth are brand awareness, the ability to find the right marketing channels for their target customer base and the costs associated with advertising, alongside competing against more established large corporates for a market share. Challenges in the supply chain are also top of mind for many leaders.Scaleups are at the heart of the UK’s trade ambitions. 57% of scaleups export and 65% want to do more in the future. The EU remains their largest market but an increasing number are looking to other markets. However, more support is needed. They want better introductions to buyers in overseas markets, more information of market opportunities, a single point of contact for scaleups at DIT in the UK and overseas and dedicated trade missions. Following the end of the transition period, 60% of scaleup leaders consider Brexit has had a negative impact on their business however this has not dampened their growth ambitions.

- Access to Talent is dialling up as a challenge once again, when scaleup leaders were asked for their number one priority accessing the skilled individuals was cited by 1 in 3, more than any other challenge. Finding the right talent, whether this means young people entering the workforce, recruiting from overseas or developing and retaining existing staff, scaleups have consistently highlighted this as a major barrier to growth.Scaleups offer internships and work experience and employ individuals from school leavers to post-graduates, however they are seeking greater support to take on new employees and ensure that they possess the right mix of skills and attributes: 56% would value grants for taking on trainees and 52% seek improved careers advice about the opportunities that exist in companies like theirs. There is also a desire to see improved connectivity with the education system through entrepreneurial education, encounters with students, vocational courses and enhanced accreditation of digital skills. Once again in 2021 technical and social skills are the most desired from school leavers and graduates joining the workforce. Critical thinking is the most desired future skill, in demand by 70% of scaleup leaders followed by cognitive flexibility. However only three in ten are confident that they will be able to source employees with these vital skills in the future. When seeking to upskill their own teams, 75% of scaleups rely on expertise from within their own company to deliver in-house training, with 5 in 10 looking to mentors and private courses for external skills development.

- Access to finance and growth capital has remained a priority in 2021. Scaleups continue to be far more likely to use external finance than their SME peers: 82% of scaleups use external funding as part of their growth strategy, although 45% still feel they do not have access to the right funding for their needs. Perceptions of regional disparities persist; similarly to 2020 four in ten scaling companies feel that the majority of funding resides in London and the South East (compared to five in ten in 2019). Of those using external finance, 5 in 10 are using equity or plan to use it in the near future – with VCs and Angels identified as the key sources of equity provision.

- Building leadership capacity through local support continues to be seen as a challenge for some however as with 2020 it appears that this demand is being met more fully. Just over half of scaleups (55%) have a Board or similar governance structure and a further 12% have plans to establish one in the future. However, scaleup leaders want greater access to networks of NEDs, they are also looking to develop their top teams seeking key skills around strategic planning, business development, sales and marketing. Being part of a network with their peers is valued as a form of support. Scaleups are also looking for support for innovation and R&D from Innovate UK and the wider public sector. These continue to be their number one asks. The majority of scaleups wish to be relationship managed, with proactive engagement and contact and a specific scaleup website. Six in ten scaleups want a named single point of contact as a local relationship manager.

- Infrastructure – scaleup leaders consistently indicate the importance of infrastructure – space to grow – as critical to their business, alongside good broadband. 1 in 10 scaleups have opened new premises or moved to larger facilities in 2021. The role technology plays in supporting hybrid models of working will continue to be important as many scaleups seek to implement new remote working practices with 56% planning to allow staff to split their time between home and work in 2022 more than doubling pre-pandemic levels (22%). Connectivity between different players in the scaleup ecosystem is vital for growth as is access to facilities and expertise for R&D at large corporates and universities. Hubs at which scaleups can work, meet and collaborate are seen as vital to a thriving scaleup ecosystem.

CONTENTS

Introduction 2021

Chapter 1 2021

The ScaleUp Business Landscape

Chapter 2 2021

Leading Programmes Breaking Down the Barriers for Scaleups

Chapter 3 2021

The Local Scaleup Ecosystem

Chapter 4 2021

The Policy Landscape

Chapter 5 2021

Looking forward

Annexes 2021

Scaleup Stories 2021

Share